In our previous Reader Story, we met Jack, an investor from Illinois who had been p2p investing since 2008. Today we have another solid interview with Jason from Detroit, Michigan. The purpose of these stories is to add a bit of emotion and humanity to this often-dry online investment, helping to further engender trust towards peer to peer lending as a viable investment for everyday Americans.

Since Michigan does not yet allow investors on its primary platform (this should change after Lending Club’s IPO), Jason invests completely through the Lending Club Foliofn secondary market. This means his start is a bit more complicated than most, and is thus a more detailed account for us to read today.

This Reader Story is particularly interesting, largely because Jason works in the banking industry. He has a keen sense of how finance works – how investments should be taken on and managed. Jason came to the proper best-practices of peer to peer lending (diversification, risk-tolerance, etc) completely through his own research and expertise, and in this way he speaks with a much-needed fresh perspective.

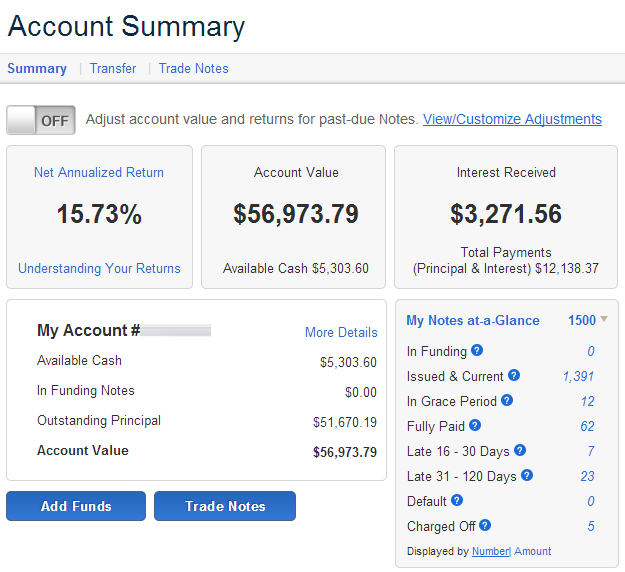

A screenshot from Jason’s Lending Club account

Interview with Jason: a Foliofn-only Lending Club Investor

Hi Jason. In a sentence, where do you live and what do you do for work?

I live in the Metro Detroit area and am a management consultant in banking.

How did you discover peer to peer lending?

I’ve always been interested in finance and different ways to invest. Wandering through the abyss of the internet, I stumbled upon a blogger experimenting with Lending Club and peer to peer lending. The guy gave an overview and discussed the pros and cons, and I was intrigued.

What convinced you to take the plunge and open an account?

Opening the account wasn’t the hard part, nor was funding the account. It was investing in loans.

I have studied stocks, options, and other investment derivatives and have always had an interest in investing, whether in the stock market, real estate, or otherwise. I have always been interested in ways to make my money work for me rather than always working for money. But when I opened a Lending Club account with $500, I didn’t quite know what to do. I didn’t lose anything, but I certainly didn’t make anything either. It took me 6 months before I touched the account again.

After some introspection, I realized I was scared and intimidated. I did not fully understand the asset, the platform, or the vast amount of information staring back at me from the computer screen.

I decided I needed to figure it out by putting some money on the line, so I dove in, committing another $1000 and several hours of time. If stock investing taught me anything, I knew diversification was key, not only across credit grades, but also across borrowers. After a quick review of Lending Club’s historical stats, it was clear that I should stick to C-F grade loans and buy no less than 200 mutually exclusive notes (i.e. not originating from the same loan). Sold.

Principal and interest began to trickle into my account day by day. It became exhilarating.

I frantically checked the account every day. Principal and interest began to trickle into my account day by day. It became exhilarating. Every day I could see my earned interest go up. People were paying and paying on time; it was working!

After some time I became comfortable with understanding the secondary market pricing, mark-up rates, yield calculations, and many other factors necessary in evaluating loans to invest in. Within the next 6 months, I went from an asset base of just $500 to over $50,000 (see the graphic above).

What is your return today? Are you happy with it?

I invest on Lending Club’s Foliofn secondary market due to the fact that I reside in Michigan. After about 9 months of investing, my Lending Club calculated NAR is approximately 15%, and around 10.2% as calculated with the XIRR methodology (as recommended by LendingMemo.com).

In order to maximize my returns, I implement a few strategies that I refer to as:

- Targeted Filtering (how I buy notes)

- Proactive Portfolio Management (how I hold/sell notes)

For Targeted Filtering, I focus on five main things:

- Yield: greater than or equal to 17%

- Loan term: 60 months

- Markup: 1% or less

- Remaining payments: 54-60 months

- Note value: $150 or less

First, a high yield ensures a good return. The difference between yield and interest rate (APR) is that once a loan has been issued and has begun to repay the debt, the effective interest rate changes; this is its yield. A high yield means high returns.

The second is a note’s term. In general, 60-month loans carry a higher interest rate. Additionally, 60 months gives the borrower more runway to make their payments.

Third is a note’s markup. Markup is the premium you pay to buy a loan. Simply put, you don’t want to pay money; you want to earn money.

Fourth is the number of remaining payments. In my experience, it is better to hold a young loan because I assume the borrower is prepared to begin making payments immediately. As time goes on, it becomes more likely that the borrower’s circumstances change and they are unlikely to repay.

Fifth is the note’s value. Generally you want to keep this to 1% or less of your portfolio, but for me, I don’t like the idea of losing more than $150 on any one borrower in the case they do in fact default.

Regarding my Proactive Portfolio Management, the analytical engineer in me got a little carried away and build an Access database in which I am able to download Lending Club data and query loans based on my criteria [Ed: awesome].

In particular, I focus on four key areas:

- Months elapsed: I sell off anything older than 15 months.

- Note exposure: I ensure that any one note does not represent more than 1% of my portfolio; diversification is key.

- Ability to repay: I calculate the borrower’s loan payment to monthly income ratio, review their DTI and income, and with that in mind, make a decision to sell or hold; this one is more of a gut check.

- Inquiries & loan purpose: Compliments of LendingMemo.com, I’ve recently begun to consider the number of credit inquires and loan purpose in my queries to further filter out potentially problematic loans.

What does your family or friends think of your investment?

I have only shared this with a few people. Some seem interested, yet hesitant. My guess is because it’s a fairly new asset class and is unfamiliar to them.

Has anything been disappointing or unexpected?

The only disappointment as of now is the limited number of states from which you can invest. I’m in Michigan, so I’m limited to the Foliofn platform. Don’t get me wrong, I love the secondary market. However, I would also like to use the main Lending Club platform and tools.

What would you say is the best part about peer to peer lending?

The three best reasons are the ease of access, the low transaction costs, and the predictability.

In reflecting on my stock market investing, I find peer to peer lending far more straightforward. Investing in stocks tends to require hours of research, comparing P/E ratios, following market trends, and even after all of that it still feels like a crap-shoot. The volatility alone is not for the faint of heart.

With peer lending, you know what you’re getting and it is relatively predictable.

But with peer lending, you know what you’re getting and it is relatively predictable. You buy a loan and the borrower pays you back at a fixed rate for a fixed term. It is all pretty straight forward. The market is governed by only a handful of parameters, compared to the stock market, which is affected by far more variables.

Obviously peer lending is not without its risks. People default and life happens. But peer lending is simply a numbers game; diversify broadly, target credit bands, manage appropriately, and you should have a fairly good chance at generating a solid return.

Thanks Jason.

Share Your Story (and Get Coffee by Mail)

Getting spotlighted on LendingMemo is simple (and comes with a bag of Stumptown). Just answer the following questions:

Getting spotlighted on LendingMemo is simple (and comes with a bag of Stumptown). Just answer the following questions:

- In a sentence, introduce yourself, your family, where you live, and what you do for work.

- How did you discover peer to peer lending?

- What convinced you to take the plunge and open an account?

- What is your return today? Are you happy with it?

- What does your family or friends think of your investment?

- Has anything been disappointing or unexpected?

- What would you say is the best part about peer to peer lending?

Email your answers to readerstories (at) lendingmemo.com with (1) a picture of you or your family and (2) a screenshot of your Lending Club or Prosper home screen. Bonus points if you’re of retirement age – we need more of you.

Indeed, the national climate will change through stories like these. If you care about spreading the word of p2p lending, let’s hear from you!

Thanks for this interview with someone who buys notes because they are outside of approved state list. I’ve always wondered if there were many people out there doing the same thing.

Any idea on numbers of users like Jason?

Hi JJ. I honestly have no idea. I know there are thousands, but as for the ballpark figure, this would be something I would love to ask Lending Club next time I sit down with them. Great question.