A lot has been written about diversification in peer to peer lending, including on this site (see here & here). In short, it is the most important thing investors need to do. Beginner investors sometimes pay too much attention to the details of each individual loan, occasionally forgetting to simply diversify their investment across hundreds of loans. Those who are frustrated by mediocre or negative returns months later, those who feel betrayed, turn, and publicly damn this entire asset class, are almost always investors who simply failed to diversify their initial deposit in enough loans.

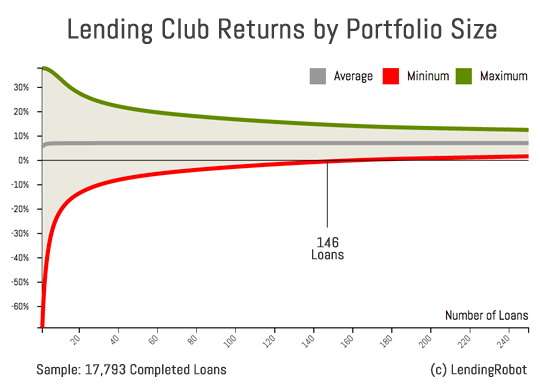

The somewhat more debated issue within peer to peer lending has been the threshold at which a portfolio of p2p loans becomes fully diversified. Basically, how many notes does it take? To explore this concept, I reached out to Emmanuel at LendingRobot. He had previously published the below chart that analyzed the completed loan pool at Lending Club.

His data showed the historical crossover point was 146 loans. Basically, (almost) every investor who diversified in 146 equally-valued notes from Lending Club’s pool of completed loans earned a positive return (note: not a guarantee for future performance).

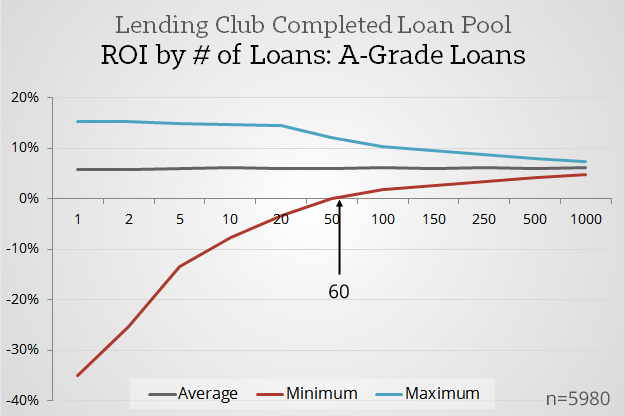

I contacted Emmanuel last month to ask if this point of diversification varied by loan grade. My thinking was that lower risk A-grade loans were probably more stable in their repayments, so the minimum note count to be diversified had probably been historically lower than the other grades. What transpired was a longer email conversation, with the result being the charts seen below.

Probably the most interesting thing this data does is add a bit more nuance to the traditional tenet of 200 notes (Orchard) being the ideal threshold of diversification. As seen in the data below, this number may be overly generous for the safer grades, and too conservative for riskier graded portfolios.

Breakdown of Historical Diversification Points by Loan Grade

Lower Risk Grades

This chart shows that investors who diversified across 60+ completed A-grade loans at Lending Club earned a positive return. This may be incredibly interesting to people like myself who are advocates for others to enter this asset class, since it could offer new investors a much lower trial investment. For some prospective investors, an initial investment of $5000 (200 x $25 notes) is a big pill to swallow. However, if we suggested prospective investors try peer to peer lending with half this amount, perhaps $2,000 (80 x $25 A-grade notes), the trial investment is palatable for a greater number of interested people. Peter Renton actually suggests something similar in his $500 trial investment post.

I imagine the underwriting at Lending Club has improved since these early loans, so this point could be even lower today.

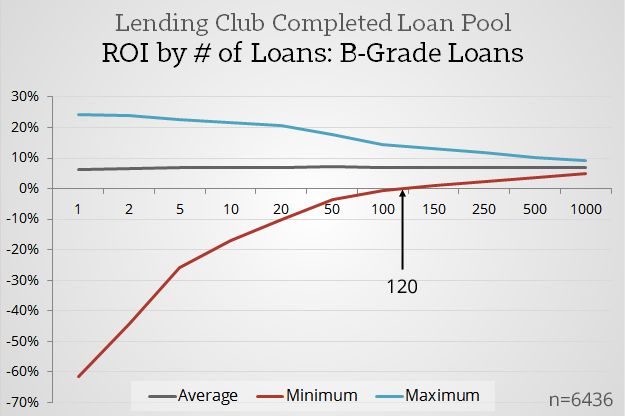

Medium Risk Grades

Here we see the point of positive returns climbing. Within B-grade loans, it is 120 loans. Again, this data indicates that less than 200 notes seems allowed for trial investments as long as a lower degree of risk is taken on.

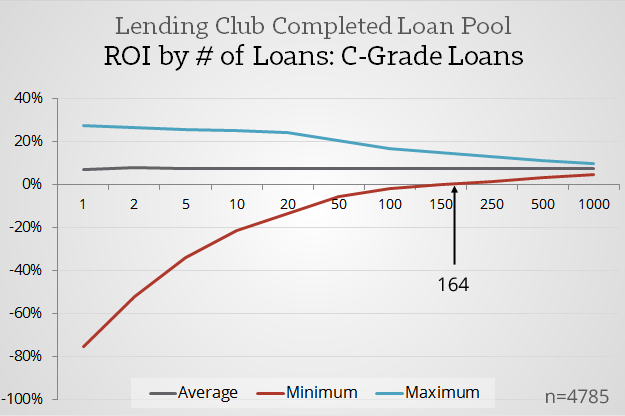

The overall point of positive returns for all of Lending Club’s completed loans is 146. Finally, in C-grade loans, we have crested this number at 164 and begin to slope downward in any further grades, needing more loans than average for diversification.

Higher Risk Grades

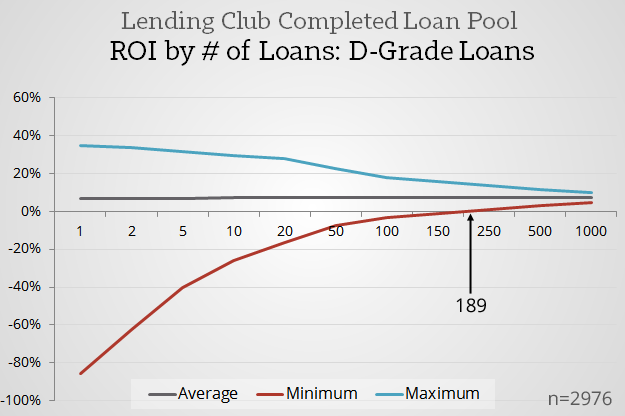

D-grade loans, similar to C-grades, require more loans than average to have an historically positive return: 189.

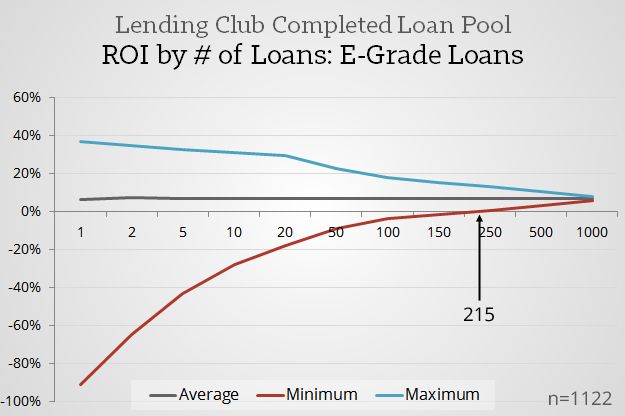

This is probably my favorite chart of the bunch. Within E-grade loans, we see that 215 notes have been historically required for an overall positive return. This is more than the conventional figure of 200, and points to the fact that diversification is more complicated than typically assumed.

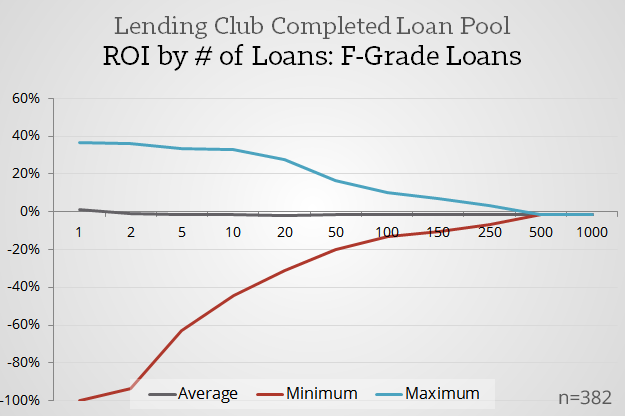

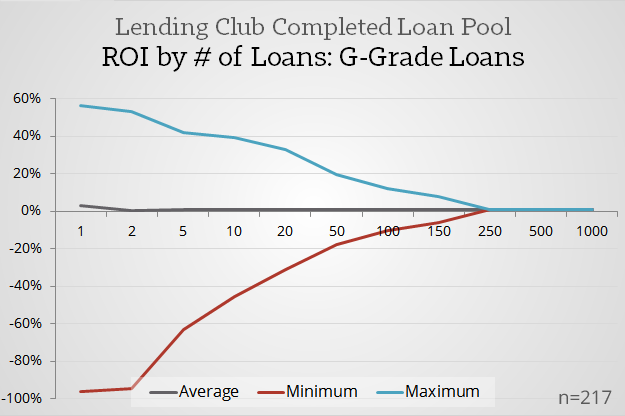

F and G-grade loans never hit a positive minimum threshold. Keep in mind that the note count has also become very low (just 382 & 217 completed loans).

Reflection: Diversification is Complicated

This post really is not a game changer. For new investors who are just starting to invest in online loans, a threshold of 200 notes remains a wise place to begin. However, it seems that prospective investors who are just wanting to try this asset class for a season could open an initial portfolio of fewer notes than 200 – perhaps just 80 equally weighted A-grades, or 150 equally weighted A & B-grade notes. Furthermore, if a new investor is focusing solely on higher-risk loans, 200 notes may not be enough. A better idea might be to shoot for an initial investment of 300 notes or more.

Hearty thanks to Emmanuel Marot and the LendingRobot team for providing these figures.

[image credit: Bob Doran “wildchick17.JPG” CC-BY 2.0]

Great post, as always. The information on the G & F notes is… priceless.

Thanks for stopping by Hunter.

Looking at the chart above for ROI on F graded loans, it appears that almost any number of F loans results in an average negative ROI. Maybe I’m wrong, but that doesn’t seem possible. I know the higher risk loans have a higher rate of default, but according to the stats on LendingClub, they also average the highest ROI even after factoring in the default rate. Thanks.

Hi Mike,

As you can see in this NSR breakdown, F and G grades do indeed have a net loss within completed LC loans: http://www.nickelsteamroller.com/#!/link?l=74f321674bb2118e9c07fab3114d2344

This doesn’t mean it was impossible to earn a positive return investing in just F-grades within this vintage. I’m sure many people did it (perhaps with some solid filtering). However, the average experience of the users within this grade was historically negative, no matter how many notes they held. That said, it’s quite possible Lending Club’s underwriting has improved today, and this may no longer be the case. In any regard, the note count is too small to really draw any sort of conclusions.

I have an issue with the data and graphs you are using here. I think they are inaccurately showing to your readers the actual returns they can expect investing in Lending Club today.

For instance – your “A” grade loan graph shows if you invest in 1 loan, your maximum expected return is ~15%. How can that be, when the A loans are 6-9%? If you picked the riskiest possible A loan at 9%, your maximum return is, 9%. Also, your minimum return should be -100%. If you were unlucky enough to pick an A loan that never made a single payment, you are obviously out your entire investment.

Also I noticed you only used 36 month loans for your search parameters for this data. With “n” values in the low hundreds for F and G loans (which have “n” values above 7,000 on the LC stats page) aren’t you selecting too small of a group to make any kind of accurate extrapolation from?

Hi Mike,

Thanks for your followup. The maximum line indeed runs higher than the average interest rates (for every grade, not just As), and the minimum begins above -100%, which is worth noting. I think this has to do with the Monte Carlo computational algorithm that Emmanuel used to provide this data. I’ll reach out to him and see what he says. Regarding F-G loans, you can see that the N values are correct if you click the NickelSteamroller link above, specifically for completed 36-month loans between Lending Club’s inception and three years from today’s date.

It’s worth stating that the point of this article is not to build expectation around returns, but to bring awareness to the complexity within diversification. Returns are better explained in posts like this: http://www.lendingmemo.com/peer-to-peer-lending-return/

Simon, this is a good article and I really like the breakdown by grade. The minimum # of loans to hold to guarantee you don’t lose money is something that is nice to know but is not really diversification.

I know this is a contrary view but I think holding too many notes is not good either. It guarantees that you will get some defaults if you invest in enough of loans cause you think you have to diversify in this way.

This info is great for newbies though that may be timid to invest or are scared of the lack of collateral and there’s some very convincing info here as to why its a solid investment.

Hi Stu. Thanks for stopping by, and thanks for the kind words. I completely disagree with your approach of thinking an investor can be diversified in 20 notes, but you’re certainly allowed your opinion.

I know you do and it’s because your background is in statistics and mine is in credit analysis that we differ. It’s also why enough notes for a positive return is diversification to you even though that’s not what diversification is. I sent you a private email about this. I’d like to see if the stats win or not and hope you reply to it.

Very interesting article, a much safer way than diversification is to support the loans made with real asset security, like an income producing commercial property and by taking a 1st charge over that property through a legal mortgage. If the borrower defaults on the loan then the lender has the knowledge that the property can be sold in order to redeem the loan.

A single loan that is secured offers a safer proposition than a diversified portfolio or 150 unsecured loans

To determine what the default rates are for the different grades loans, are a “random group of loans used within that grade”? I am also assuming that the default rate is compiled from an equal numbers of say, E1- E5 in the E grade.

Since many investors choose their loans to purchase, it seems that the total default rate could be improved upon, if the investor was very picky. Regardless of the grade, many loans are more appealing than others.

I have been sticking with the $25 loans and fairly stringent choices and filters.

Great article!

Stan

Thanks Stan. The default rate is compiled from all completed loans. You can see the default rate for these completed loans at NSR: http://www.nickelsteamroller.com/#!/link?l=74f321674bb2118e9c07fab3114d2344

If you want to see the default rate outside of this specific set (IE: for all loans), simply hit the “Clear” button to clear the criteria and refilter with the Filter button.

I’ve just recently started investing with Lending Club and LendingMemo.com has provided me with great information. I first started on the safe side with A and B grades and then started learning about how to be a real investor. Thanks for all the help

This is a good start and a good overview, but more visibility would help. The key to this analysis (and to arriving at an ideal number of obligors) is a function of two variables:

i) the degree of confidence (e.g., how sure you are that you will not lose more than x, in this case seemingly defined as a minimum return of 0%). This is a personal preference and gets to how risk averse an investor might be. If these numbers were determined with a 99% confidence level, it still means that an investor could lose money;

ii) The correlation between obligors (or the conditional probability that one obligor will default when another one does). This ‘input’ is almost always a fudge and is dependent on many things. For example, if one accumulates loans in one geographic area, the correlation between these borrowers is almost certainly greater than if the obligors were spread over the country (e.g., if California enters a bad recession as a result of high taxes, crazy regulations, over population…um, you get the drift -then obligors in CA might suffer defaults more rapidly than in other parts of the country).

My understanding of Lending Club is that should it go bankrupt — and its asset/liabilities numbers aren’t looking impeccable lately if I recall correctly — it doesn’t owe its investors much and will in all likelihood repay far under what the notes are worth. Would you recommend investing across various platforms as well? (LC, *and* Prosper/whatever’s out there)

Diversification is the heart of any mature investing portfolio.

Are you using filters, or are they just random notes regardless of its red flags?