To encourage more people to start investing, each quarter I post the current state of my personal peer to peer lending accounts.

Because of my age and life-situation, I am an investor who feels comfortable taking on more risk than most investors. While this means my returns are probably higher than average, the riskier loans I have also means my portfolio is more susceptible to macro economic factors, like a rise in national unemployment. Most investors are probably better off staying in the safer graded loans.

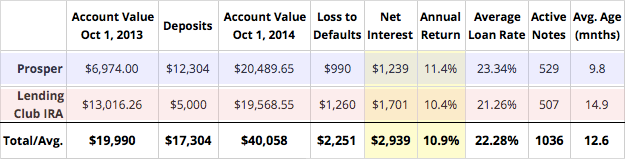

Returns for Q3 of 2014 (Trailing 12 Months)

As seen below, I continue to celebrate great returns at Lending Club and Prosper:

This is the first quarter I’ve switched to reporting my returns trailing twelve months (ttm). While this calculation results in a return 1% lower than last quarter, the change is really important. Both my personal accounts and the industry as a whole are somewhat susceptible to loan defaults, so a trailing twelve month return will be a more-accurate/less-fuzzy representation of where things stand today.

Some notes on this data:

- Account values, defaults, and interest totals are pulled from the statements that Lending Club and Prosper issue each month to their investors (See your LC Statements // Prosper Statements [login required]).

- The important figure of Net Interest, highlighted in yellow, is calculated by taking the sum interest earned for the past twelve months and subtracting that period’s total value of defaulted loans.

- Annual Return, also highlighted in yellow, is done via XIRR (see: XIRR calculator), the best way to independently calculate your peer to peer returns. Most investors will probably not need to go to such lengths, and can trust the onsite NAR figures at Lending Club or Prosper.

- With an average age of 10 and 15 months, these accounts are not yet fully seasoned. Read: The P2P Return Curve

- All returns are pre-tax.

P2P Lending Account Breakdowns

My returns dropped slightly from last quarter (see 2014Q2):

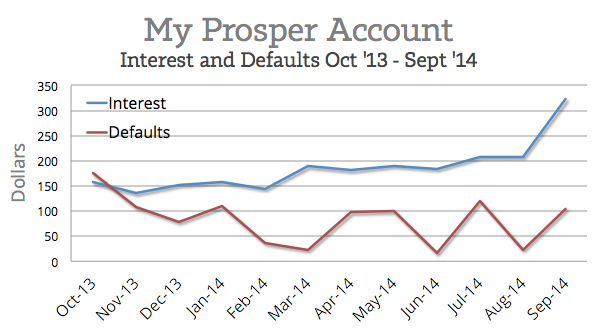

Prosper taxable account: Earning 11.4% Interest

In late July, I added $10,000 to my Prosper portfolio so that I would be equally invested in both platforms. It took a month to get this cash fully invested, but now that it’s complete I’ve started to receive more interest per month as seen below:

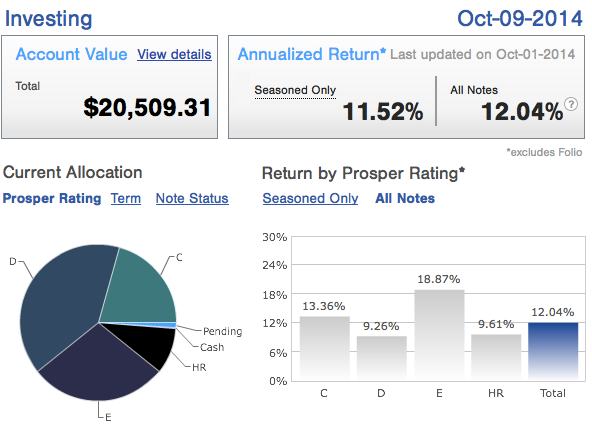

Here are additional breakdowns from my account at Prosper:

56% of these loans are 5-year; the rest are 3-year. This is the first quarter I’ve ever shown C-rated notes, though they are unseasoned. Chasing the highest return I can find, a filtered cross-section of C-rated loans seem to be better investments than many E and HR-rated loans, so I’ve tipped my account a bit higher up the credit spectrum. That said, C notes at Prosper are somewhat equivalent to D-grades at Lending Club, so this isn’t a huge shift for my overall strategy.

All in all, I’m very happy to be an investor at Prosper.

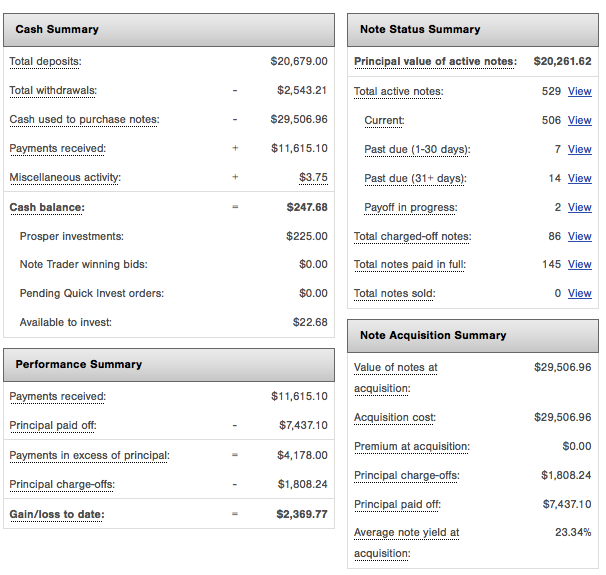

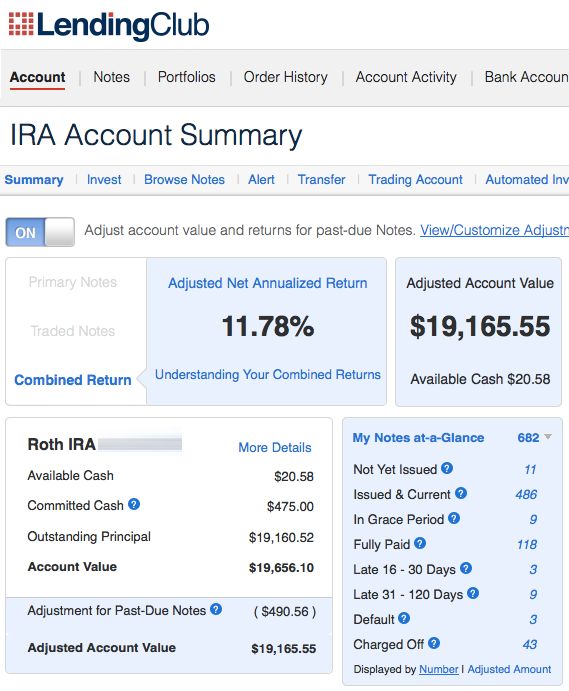

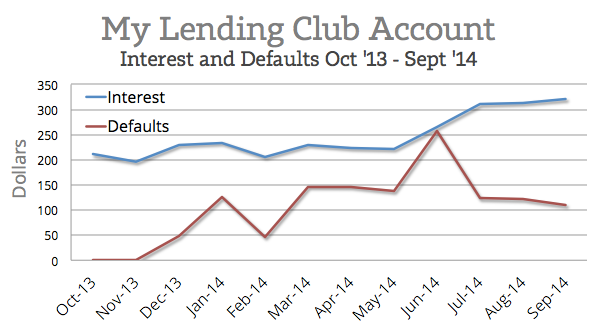

Lending Club IRA: Earning 10.4% interest

My Roth IRA continues to be a rewarding choice. Last quarter I mentioned a sudden spike in defaults, and you can see this spike in the month of June below:

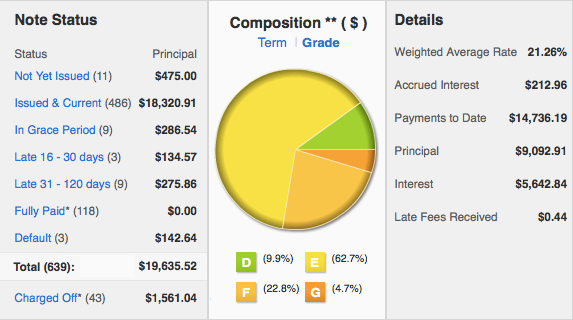

Here is another breakdown for my retirement account:

It’s great to see so few loans going late considering the near-500 active notes within this account.

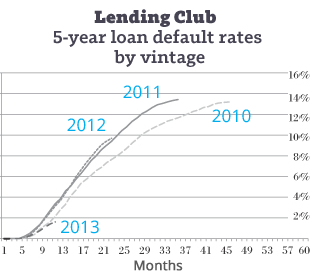

A word on 5-year loans at Lending Club

I continue to feel comfortable with the degree of risk and return of this account, but I’m also really wanting this account to fully season. Most accounts season at 18 months. However, I assume this point will be different for my account considering 90% of my notes are in 5-year loans. Lending Club only began issuing 5-year/60-month loans about 4 years ago, so we don’t really have the full picture for when they fully season. The data we have seems to show the default curve for 5-year loans flattening out around month 30 (see above graphic).

I continue to feel comfortable with the degree of risk and return of this account, but I’m also really wanting this account to fully season. Most accounts season at 18 months. However, I assume this point will be different for my account considering 90% of my notes are in 5-year loans. Lending Club only began issuing 5-year/60-month loans about 4 years ago, so we don’t really have the full picture for when they fully season. The data we have seems to show the default curve for 5-year loans flattening out around month 30 (see above graphic).

Interestingly, a comparison of the term of these loans (36/60-months) would have the same ratio as a comparison of their seasoning points (18/30-months): 0.6.

Want a Passive Investment that Earns 10% Per Year? Go P2P.

It’s true. I barely manage these accounts month by month. For the most part, the settings on the auto-investment tools are where I want them. Available cash is automatically placed into additional loans, and I am able to focus on more important things. I’m not sure if people realize how amazing this is, so let me put things in brighter focus.

Things I did this week:

- Earned 10% in my Lending Club retirement account while I ate eggs and toast for breakfast

- Earned 10% in my Prosper account while playing frisbee golf with Doug

- Earned 10% at Lending Club while vacuuming the carpets in my home

- Earned 10% at Prosper while watching a movie before bed

And the kicker:

- Earned 10% in peer to peer lending while earning actual income at my job

I find it quite something to be living life, doing the normal things that people do, while also earning a great return through investing online. The realization almost stops me in my tracks. Even now, while I compiled this article, tiny note repayments were flowing back into my accounts, ready to be auto-invested in further notes when enough of them pile up. Further, I’ve been experiencing these healthy passive returns for years, and don’t see it ending anytime soon.

Tell your loved ones. Tell your dentist. Auto-investing in loans to prime-rated borrowers is the single greatest passive investment available in our country today.

Questions/comments?

Congratulations on expanding on your investment with Prosper this summer and for the continued success at both Lending Club and Prosper. It will be interesting to watch your Prosper account now that it has two big “waves” of capital. Already the average age has been affected significantly, so you will almost be able to track two vintages of cash. Just another fun dynamic of P2P lending where the ability to analyze performance is easy to do, yet can be done from a wide variety of angles.

I will be doing a quarterly performance review of my P2P investments this month as well, so it is always good to have fellow investors to compare and discuss with. Thanks for sharing your update and for your transparency.

Thanks Adam. Looking forward to your update.