There’s hidden toxin in this investment, an unseen mud that weighs down our returns, and thousands of investors are completely unaware of it.

Of course, I’m talking about cash drag, the negative effect that idle uninvested cash has on our overall return. All of us have a cash balance in our peer to peer lending accounts throughout the day, so cash drag affects all of us in some way or another. However, those who are aware of it can take great steps to minimize its effects.

Probably the best way to demonstrate the dangers of cash drag is seen in the Net Annualized Return (NAR) figure provided by these platforms. Many investors are not aware that these return percentages only apply to invested cash.

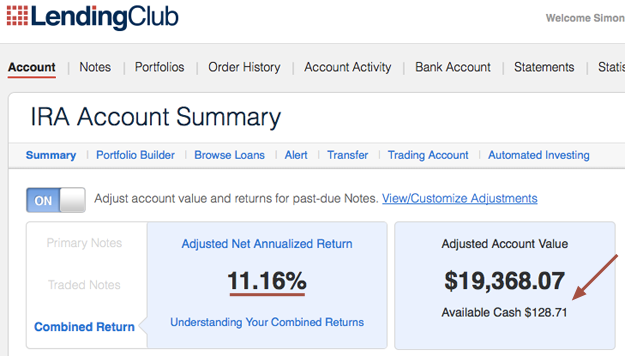

Here is the main screen of my Lending Club account (see my returns). As you can see, it tells me I’m earning 11% percent per year, which would make me feel pretty good about myself if it were true. However, these gains only apply to funds that are currently invested in loans. The available cash in my account (see the arrow) is not figuring into this return.

For example, say you want to begin investing at Lending Club so you transfer over $5,000, but you only invest $25 in a single note. Your NAR might say you’re earning 8% return on your investment. But $4,975 would be just sitting there earning no interest at all, and if you include this idle cash in your equation, your actual return would be closer to 0.1%.

If you want a calculation that includes idle cash, I suggest XIRR.

For investors who want a calculation that includes idle cash, I suggest they try XIRR. LendingMemo’s XIRR calculator is actually really great at giving a more holistic measure of your returns that is not just based on note performance, but by how much money you have deposited and withdrawn in your account over time. Read more: Calculating Returns via XIRR

This isn’t to say the NAR figure is worthless. The fact is, many seasoned investors actually prefer it. Here’s a quote by Jason in Detroit about why he prefers NAR over XIRR:

“Including cash with invested funds (XIRR) is an apples to oranges comparison, given that cash is risk-free, while loan investments are exposed to the risk of defaults and charge-offs. By incorporating the cash value of one’s account, you might as well include one’s entire checking account balance, as that is also idle money that could be invested.”

Jason’s point is a great one, and reminds us that XIRR should not be used in isolation. However, even Jason would agree that investors need to be aware of the negative effects of cash drag, and by holding up NAR and XIRR side by side, we can see this effect plainly. IE: my personal Lending Club NAR is 1% higher than my XIRR percentage, and this lost percent is mostly the fault of cash drag.

How do we fight this factor? Keep available cash low.

The fight against cash drag is never ending and will always bring down our returns in some way or another. However, we can fight it by doing one simple thing: keeping our available cash as low as possible. This is done in one of two ways:

- Reinvesting idle cash into more loans

- Transferring it out of our account altogether

Idle cash earns no interest.

The point is that idle cash earns no interest, nor is it a good avenue for spending like a checking account, so it needs to be put elsewhere. Whatever the case, the lower we can keep our idle cash balance, the smaller negative effect that cash drag will have on us.

If Cash Drag is the Problem, Automated Investing is the Solution

Thankfully, both Lending Club and Prosper have implemented really helpful solutions to fight against cash drag: automated investing. A quick setup on either platform, and any available cash that builds up in your accounts will automatically be invested into additional loans. And both of these automated options are completely free to use.

I’ve personally enabled the automated investing features in both my p2p lending accounts, and can attest to how good they are at keeping our cash balances low, particularly for more common grades like As, Bs, and Cs. Indeed, these tools make peer to peer lending a near-passive experience!

Automated Investing: Lending Club

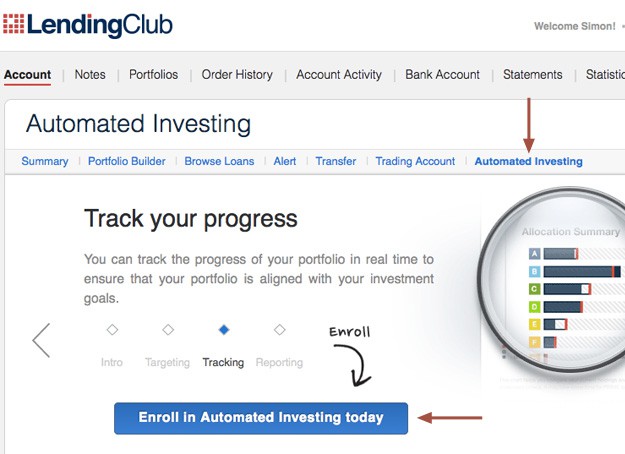

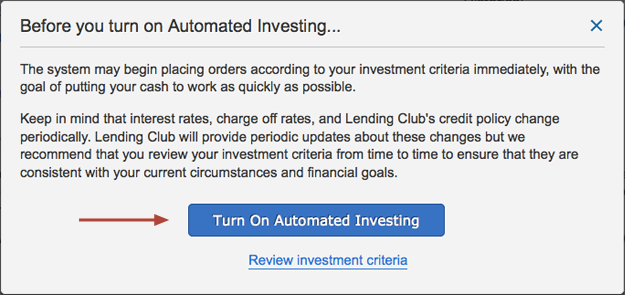

Lending Club’s automated tool is excellent at putting available cash to work. You can find the tool under the Automated Investing link in the navbar. Clicking on it will bring you to the signup screen below:

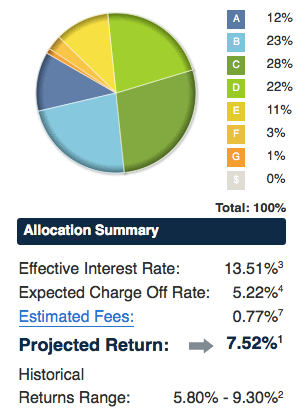

Clicking on the Enroll button, you will arrive at the main Automated Investing area. The top of this page is dedicated to choosing the level of risk for your investing:

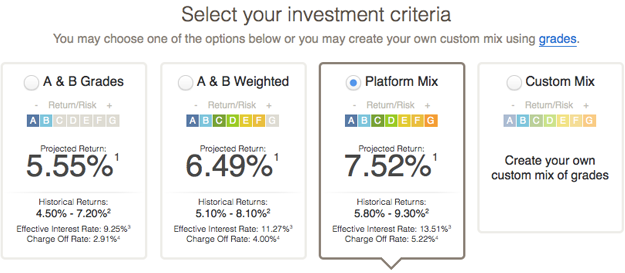

Lending Club offers three of their own allocations (A & B, A & B Weighted, and Platform Mix) as well as the ability for you to create your own custom mix of loan grades, with a projected return beneath each of these allocations. Auto-investing in safer A and B-grade loans will result in a safer investment that is less likely to experience defaults (for example, if the national economy goes bad). However, the returns for safer grades are much lower than the rest. Choosing the right level of risk for your investing is really important, and is fully explored in this article: “Risk Tolerance 101: What Loan Grades Should I Choose?”

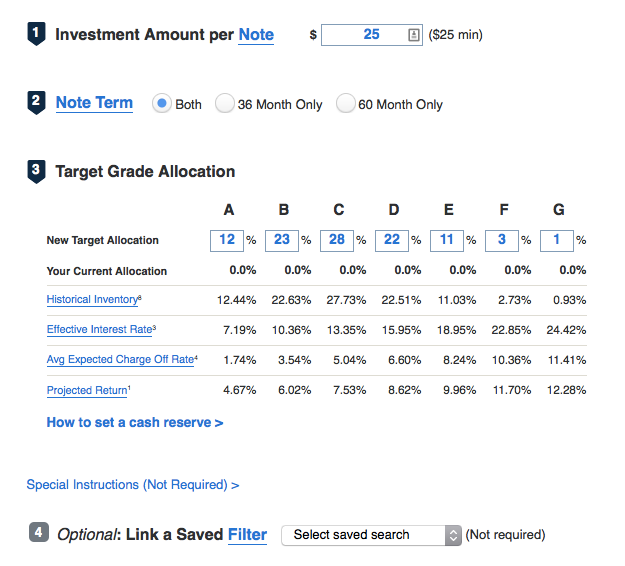

Looking farther down on page, you’ll find a more detailed breakdown of this tool. Lending Club has helpfully added a 4-step process to this area:

- Investment amount per note: here you select the right note size for your automated investment. Most investors need to spread their investment across 200 notes to be fully diversified, so those with $5,000 to invest should use $25 notes (25 times 200 = 5000). Those with $10,000 to invest can use $50. Those with $15,000 can use $75, etc.

- Note term: choose either 60-month (5 year) or 36-month (3 year) loans. This is another area to take on or decrease your account’s risk/return. For a safer investment, stick with 3-year loans. Want higher possible returns? Take on more 5-year loans.

Target grade allocation: here you can adjust what percentages you want in each loan grade and watch the pie chart adjust accordingly. So if you like the Platform Mix setting above but want more risk than it offers, you can move the percentages around for your particular needs. Interestingly, you can keep a portion of your account in cash if you keep the overall percentage under 100%. So if all my grades combined only equal 95%, Lending Club will make sure 5% of my account remains in cash. Note: the tool may have trouble finding loans for you if you place too much emphasis on rarer loan grades (E-G grades).

Target grade allocation: here you can adjust what percentages you want in each loan grade and watch the pie chart adjust accordingly. So if you like the Platform Mix setting above but want more risk than it offers, you can move the percentages around for your particular needs. Interestingly, you can keep a portion of your account in cash if you keep the overall percentage under 100%. So if all my grades combined only equal 95%, Lending Club will make sure 5% of my account remains in cash. Note: the tool may have trouble finding loans for you if you place too much emphasis on rarer loan grades (E-G grades).- Link a saved filter: if you want to invest with a filter, which is often a sensible option, click the Special Instructions link and select one. Remember that stricter filters may not always find the loans you need. Read more: My Personal Filters for Lending Club

That’s it! Click the Save your Criteria button at the bottom and click the blue button that pops up. Congratulations, your account is officially automated. Any available cash will be invested in additional notes throughout the day, spread across the grade percentages you set up.

If you ever want to disable automated investing, you can do it easily by going back to this page and reclicking the blue button that says Pause Automated Investing.

Automated Investing: Prosper Marketplace

Automated investing at Prosper is a little more complicated, but still quite doable. It requires you to first create a “saved search” (a filter), and then set up that search for auto investing in more loans.

Step #1. Create a “saved search”

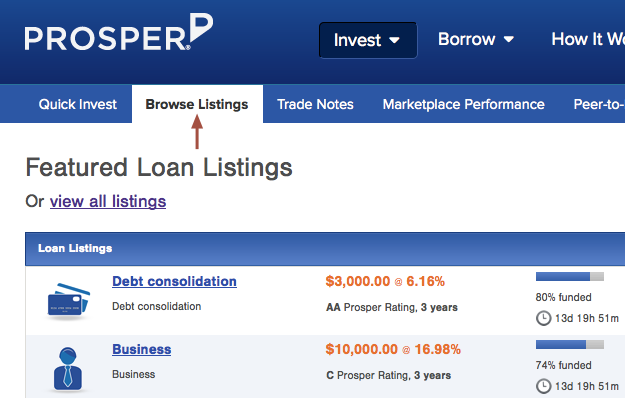

Do this by navigating to Prosper’s Browse Listings page:

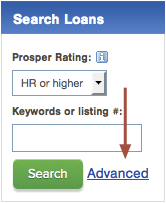

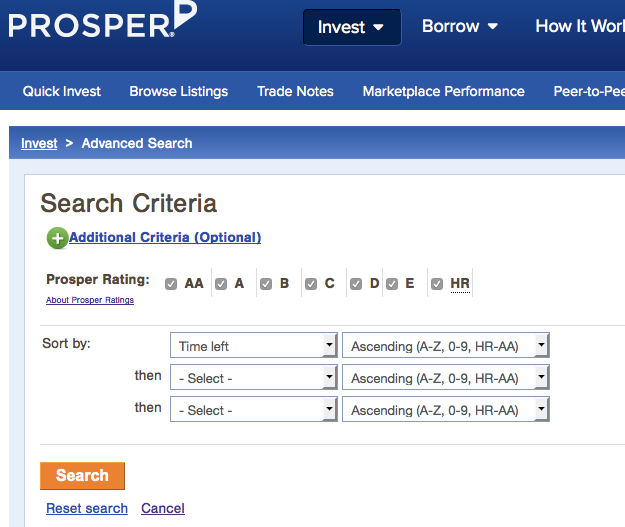

On this page, you can navigate farther down, past their list of available loans, to find the Search Loans box, seen on the right. Although this box is primarily used for sorting Prosper’s available loans by grade, we’re much more interested in the Advanced link located in its bottom right. Click this link to be brought to the Advanced Search tool as seen below:

On this page, you can navigate farther down, past their list of available loans, to find the Search Loans box, seen on the right. Although this box is primarily used for sorting Prosper’s available loans by grade, we’re much more interested in the Advanced link located in its bottom right. Click this link to be brought to the Advanced Search tool as seen below:

To create a saved search, select your risk tolerance through choosing one or more Prosper Ratings (AA-rated are safest, HR-rated are riskiest). The level of risk you choose is one of the more important decisions you will face in peer to peer lending. Read more about it here: “Risk Tolerance 101: Which Loan Grades Should I Choose?“. You can also add additional filtering factors (like excluding borrowers with a recent inquiry) through the Additional Criteria link.

When you’re all set, click the Search button and you’ll come to the results page.

(click to enlarge)

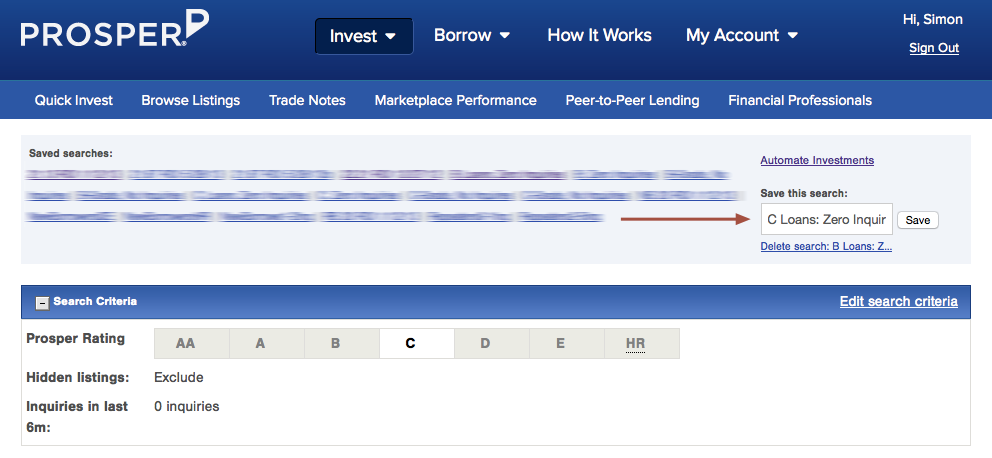

On the results page, give this search a name and save it for future use.

Step #2. Automate this “saved search”

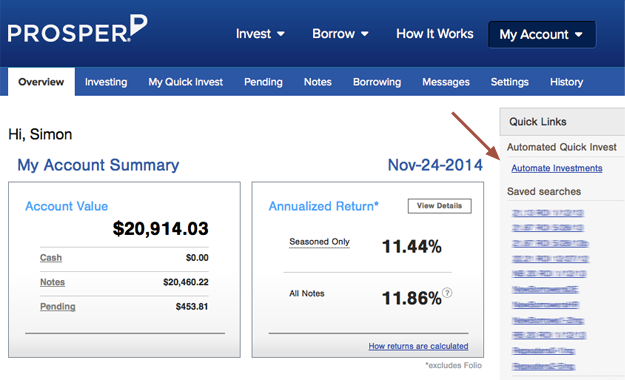

Now that you have saved this search, you can have Prosper automatically invest in loans with it by enabling their Automated Quick Invest tool. You can do this by clicking the Automate Investments link in the above screen, or by clicking this same link on the main account page:

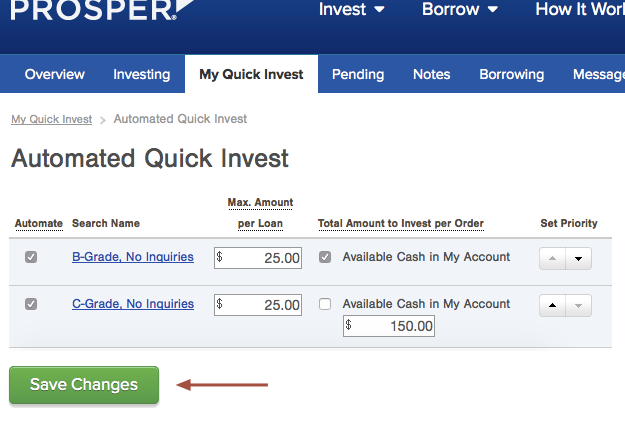

This link will bring you to the Automated Quick Invest tool, seen below:

To automate your Prosper investment, do the following:

- Click the box next to each Saved Search you want to use

- Set a note size, seen in the ‘Max. Amount per Loan’ column. You will need to choose a note size that allows you to diversify in 200 notes or more. Investors with $5,000 will use $25 notes ($25 times 200 notes equals $5000), investors with $10,000 can use $50 notes, etc.

- Choose how much to invest under the ‘Total Amount to Invest’ column. Most investors will use any available cash, but if you want to set a specific max per order, that works too. In this example, I set the first search to use up available cash, and the second search to only invest a max of $150 per order.

- Finally, set a Priority for each search that dictates which Search gets first dibs on your available cash. IE: if I only had $25 in available cash, the top filter would grab this money before the second filter.

That’s it! Hit the green ‘Save Changes’ button at the bottom and you’re officially an automated Prosper investor. If you ever want to turn off automated investing, just navigate back to the Automated Quick Invest page, uncheck the box of the search you want to disable, and click the ‘Save Changes’ button.

Avoid Cash Drag with Manual Investing

If you don’t feel comfortable handing the reigns of your investment over to Lending Club or Prosper, you can still keep idle cash low without enabling automated investing. However, you will need to set up a schedule or rhythm where you regularly log into your account and put that extra cash to work. It can be helpful to invest during the hours when new loans are added to the platforms, since more loans are available than normal. Lending Club adds new batches of loans to their platform at 6am, 10am, 2pm, and 6pm PST. Prosper does this at 9am and 5pm each day (noon on Saturday/Sunday).

For many investors, logging in once per week is enough.

The more often you log in and put cash to work, the less cash drag will bring down your ROI. But few want to sit on these websites hour after hour, so you’re going to have to find the correct time span that is right for you. For many investors, logging in once per week is enough. However, your needs may be different.

Note: Investing Lump Sums Can Be a Challenge

If you’re brand new to this investment, and have a large lump sum you’ve moved over, the problem of cash drag can be especially apparent. New investors typically transfer over $5,000 or more, and it may take a while to get that lump sum completely wrapped up in loans.

For new accounts, the automated investing tools are probably not the complete solution, particularly if you’re investing in the riskier D-G grades at Lending Club (C-HR on Prosper) that are rarer in number and thus are higher in demand. In these situations, I recommend people supplement their automated investing with manual investing, at least until the initial lump sum is completely put to work (see the times above). Once the lump sum is put to work, automated tools can be all an investor needs to keep newly available cash invested into additional notes.

[image credit: NeilsPhotography “Stuck in the mud” CC-BY 2.0]

Was hoping to read your thoughts on 3rd party automated investing websites. I use lending robot currently because it uses my preferred loan profiles and looks for matching loans within seconds of when the post. The service is free below $10000 managed and it links to both platforms. I’ve heard of some other automated services too like bluevestment (sp?). Do you have any thoughts on the subject? Cheers!

I would also like to know Don. Previous articles earlier this year from Simon was very pro LendingRobot but lately I get a feel that has changed? The automated investment tools of LC and Prosper is not good at all (as of June this year). So unless they made some crucial enhancements, why not go with Lending Robot versus LC/Prosper?

Hi Leon (and Don),

I’m still very “pro” toward auto-investment tools like Lending Robot. However, I find the easiest solution for new investors is indeed Lending Club’s onsite automated tool. I’ve been using it for quite some time and feel it is adequate. For beginners.

For people using stricter filtering criteria, the tools are obviously a better way to go. But this article is for “P2P Lending Basics”, and new people are probably fine with Lending Club’s own tool.

Prosper’s works less well unless you stick with the popular grades, but I threw it in here for good measure.

Simon, thanks for a great piece on cash drag! For anyone familiar with our toolset, it’s obvious why we appreciate this so much. It was this exact problem that was one of the primary inspirations for the creation of notient. After really getting into investing in P2P loans, we saw how much money we were leaving on the table but we weren’t satisfied with some aspects of the built-in automation tools on Lending Club and Prosper. Although the automated investment features on Lending Club and Prosper are certainly better then leaving your cash idle, as is often the case with original product features, they can be improved upon. We invite you and your readers to check us out and create and use an account (for free) at https://notient.com

This tool is also available for Lending Club: http://www.p2pinvestorkit.com