Note: this is an outdated post. My latest returns for 2014 are here.

Each quarter I post the current state of my peer to peer lending accounts. I am a lender who enjoys maximizing my return through fine-filtering available loans with the highest interest I can find.

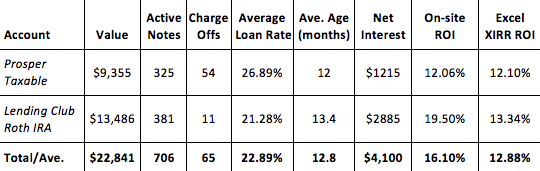

As you can see in the following table, I continue to celebrate positive returns on both Lending Club and Prosper.

Figuring Out ROI Can Be Tough

Calculating your peer to peer lending ROI (return on investment) is tricky business. If you want the easy route, both Lending Club and Prosper offer you their sometimes inflated number. Calculating your ROI with XIRR through Excel is probably the best, but this still does not take into account any notes that have gone late (and are, as such, no longer worth their full value). Michael’s Portfolio Analyzer at NSR includes a reduction from these late notes, but does not do well with loans bought or sold on the secondary market (which I have done many times). I have included on-site and XIRR ROIs for comparison’s sake (see my analysis of calculating XIRR return).

Accounts Breakdown

Prosper Taxable Account: 12.1% ROI

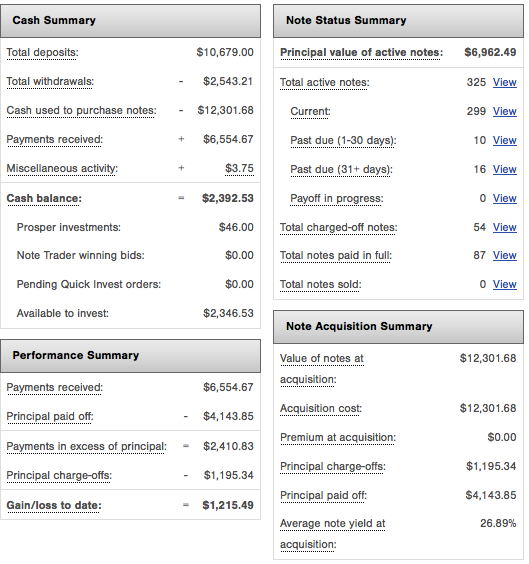

Prosper Account 2013 Q4 (click to zoom)

As you can see in the top table, the average interest rate on my Prosper loans is close to 27%. Yet, my overall ROI is 12%. This is the result of the 54 defaults this account has suffered, all from investing in this riskiest group of p2p borrowers available – I only invest in E and HR-grade loans. Not even Lending Club offers access to this borrower population.

The theory I have been pursuing is that this higher initial interest rate would propel my overall ROI higher than most investors. While this tactic has certainly been fruitful (12% ROI is fantastic in this market), it is lower than I was shooting for. The idea was that the 27% interest rates on my Prosper loans could compete with the Foliofn selling of late loans in my Lending Club account, and both accounts could stay at 15% ROI. This theory did not work out exactly as planned.

That said, my Prosper account is over a year old, and so things are slowly stabilizing. I expect this account to drop another percentage point or two, landing at an overall 10-11% return.

P2P investing using leverage: Last month I deposited $2,305 into my Prosper account. Regular readers may recognize this amount as the AA-grade loan I recently received from Prosper. As an experiment, I’m investing my loan into Prosper instead of paying it back. Considering my loan was at 7.66% and my return is 12%, I should earn a positive return overall. I acknowledge that investing with leverage is typically frowned upon, but I think this could be fun anyways. I may simply pay the loan off early if things seem awkward enough.

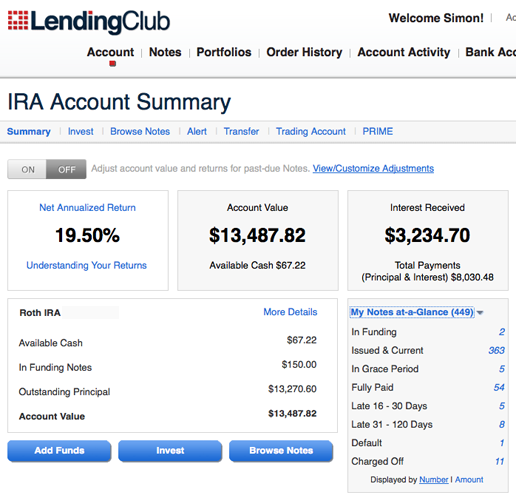

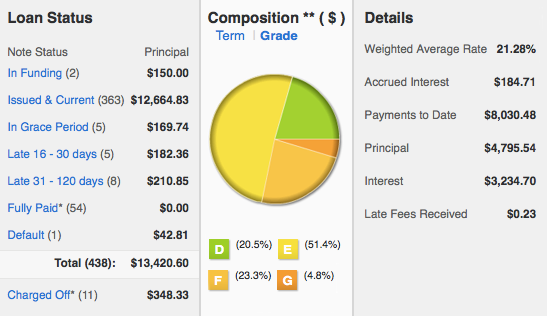

Lending Club Roth IRA: 13.34% ROI

Lending Club 2013 Q4 (click to zoom)

I continue to be proud of my Lending Club Roth IRA. It represents the bulk of what I have learned as a lender, and is fruitful as a result. You may notice that it is earning a percentage point more than my Prosper account, and this (I believe) is the result of my selling late loans on Foliofn, though I am taking a break from doing this in 2014. It seems that selling notes on Foliofn with my IRA is potentially unallowed (see this thread at Lend Academy), so I’m taking a break from it until things get sorted out. As a result, I currently have a number of late notes that typically would have been avoided.

The majority of my notes are E-grade, as seen in my average interest rate of 21%. Similar to my Prosper strategy, I try to pump up the average interest rate as much as possible, so that the return curve might place me in a final ROI that is higher than average. Currently, I feel this strategy is working, considering my Lending Club account has a 13% return and is over 13 months old. My goal is to have an XIRR return of 12% at the 18 month mark.

As a side note, 82% of my notes are in 60-month loans, a risky move considering we do not have complete data on 5-year notes, since none have been able to finish their full payments. That said, I trust the risk-wizards at Lending Club, and imagine the default rates should track similarly to the 36-month loans.

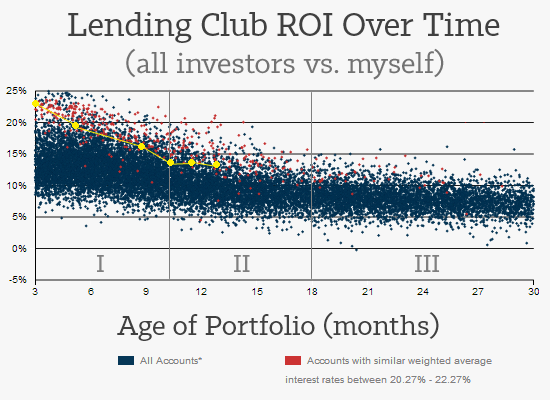

Conclusion: Riding the Return Curve

In my recent article on the peer to peer lending return curve, I highlighted how every portfolio goes through three seasons. The initial season is for the first 10 months, and is where the majority of defaults happen. The second season has defaults slow down, and ends at month 18. The final season, months 18 and up, has the most stable returns since the majority of loans that default would have done so.

As seen in the graphic above, I am doing well in comparison to the rest of the investor herd. I imagine the return will drop by another point or two, but I hope to arrive at month-18 with a combined XIRR of 12%.

Simon…Thanks for sharing your experiences and data analysis.

I am new to P2P with $10,000 invested so far within three months. The big problem I have with Prosper is the lack of availability of higher end loans. I suspect most are scooped up by institutional investors but I have no proof of that. However, for the most part I am more conservative with loans, most in the A-B-C-D categories. That translates to the 13% return area in the beginning, tapering down to 9% after the defaults start coming in (9-12 months). Frankly, given my returns in other ventures (such as I-Bonds at 5-6% for 30 years or the ups and downs of the stock market), a solid 8-9 % return is great. According to Prosper’s Data, no one has lost money with at least 100 loans as part of an investor’s diversification. My goal is at least 400 loans to begin the first year. Thanks again for analysis.

Excellent results David. This site is here to help investors like yourself achieve exactly what you’re doing. Congrats.

Very smart to track yourself against the Return Curve – I really like that! As someone who posts my own returns publicly, I may follow your lead on this one.

My own returns aren’t quite as high, but mostly because I have most of my notes in B & C grades as I’ve tried to get comfortable with the risk. I find it personally difficult to go for the E & F grade notes, even though I know the data shows they have the highest ROI. I think as I invest in more notes and start to feel a bit more diversified I’ll push myself into higher risk territory. My account is also still relatively new; even though I’ve been investing for 9 – 10 months at this point, the average age is only 4 months, since I’ve been adding and investing new cash over time. So I’m just at the cusp of what I know to be the most painful part of the default curve, where the majority of defaults occur that have the most outsized impact on an account.

Like David, I’ve set a number of goals for myself, the first being to get to 750 notes total, at which point I should have the majority benefit from a diversification point of view. I also want to get more familiar with 3rd party tools for investment. I’ve been using NickelSteamroller and InterestRadar so far, and really like them both. It remains to be seen though if they are successful at increasing overall ROI.

Wow thanks for stopping by Ben. I’m looking forward to reading more on LendingWealth.

I am curious about the 13% XIRR return rate of your LC account. The summary page showed $3234 interest received, and adjusted loss of about $600 from non-performing notes. Given the weighted avg rate of 21%, the XIRR return would be close to 16%. Did you sell a lot bad notes on Foliofn? By the way, where does the big blue dot hide?

Hi Raymond. Indeed, even though I have received a hefty amount of interest, my overall XIRR is brought down to the 13% range. I have sold a great number of grace-period notes on Foliofn, so that is probably largely to blame for the difference. As for my own blue dot, it’s not really mentionable since NAR isn’t accurate for folio sellers, but if you need to imagine it, it is 19.5% at 13 months.

I don’t think I have the guts required to ride the DEF train… I’m sticking with A and B loans. That rate of return is still pretty high when compared to things like savings accounts, etc!

Very true!