Last week I had the privilege of traveling to San Francisco and having a conversation with the two peer to peer lending platforms. Aaron Vermut, who recently changed in his title from President to CEO, had spoken in my previous interview on the transition it was undergoing from its previous management (Read: Vermut on Prosper’s Transformation into a Contender).

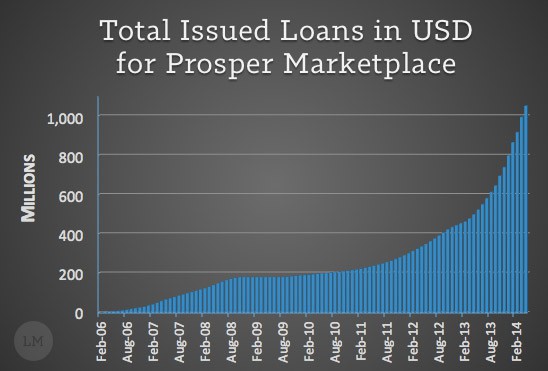

This interview was different. While still considerate of the past struggles, Vermut spoke candidly on Prosper’s turnaround being complete, how the recently crossed threshold of $1 billion in issued loans is only the beginning of Prosper’s overarching goal to transform American finance.

Interview with Aaron Vermut, CEO of Prosper Marketplace

On April 3rd, Prosper crossed $1 billion in issued loans. What is the significance of that milestone?

First and foremost, it establishes the turnaround. Last year was really about survival for this company. When our new team came in here, the company was in the low $400 million originated. Today, the majority of the loans Prosper has originated have been in the last year under the new management. Crossing that number has allowed us to put a stamp on April 3rd and say, “This is the day we turned the company around.”

First and foremost, it establishes the turnaround. Last year was really about survival for this company. When our new team came in here, the company was in the low $400 million originated. Today, the majority of the loans Prosper has originated have been in the last year under the new management. Crossing that number has allowed us to put a stamp on April 3rd and say, “This is the day we turned the company around.”

Prosper has hit an inflection point and is now making money on each loan, something that was not the case until the fourth quarter of last year. Before, our expenses were going up and our losses were also going up. But if you look at our recent quarterly statement, what you finally see is our losses going down.

Having an outstanding team has been the driver behind our success.

There are a vast number of things going on underneath the hood at this company. As I have mentioned before, this is a more complex business than I anticipated before we got here because it touches credit modeling, pricing, consumer marketing, etc. Peer to peer lending platforms are incredibly complex to operate, but having an outstanding team has been the driver behind our success.

What I think is really telling is that, while it took eight years for this company to issue $1 billion in loans, we will cross $2 billion this year as well, issuing a second billion dollars in 2014 alone.

Related to your point on these platforms being complex, would you cite that as a reason why additional platforms haven’t launched?

People have tried. But as [President] Ron Suber says, they fail to launch and launch to fail. This is a little bit like open-heart surgery. I could tell you how to do it, but you could not necessarily do it yourself. To the credit of what was here when we got here, it was a functioning platform. It was originating loans, so that gave us a lot to work with.

Do you think another platform will ever launch? Will there ever be competition besides Lending Club?

I’ll answer that question in two ways. Firstly, we have lots of competition other than Lending Club. In fact, we do not really even see Lending Club as the competition because the addressable market is so big. Lending Club and ourselves may have business model similarities, but we are certainly not the only companies who are lending money to people. The press likes to call us competitors, but there are…

… Discover personal loans.

… Discover personal loans, there are lots of other point-of-sale products and prepaid credit cards, and so on. The personal credit space is huge. Prosper lives inside the unsecured consumer credit of that space. We will differentiate ourselves through our product, service, transparency and being good guys, through word of mouth. One of the things that is really resonating now, and it has taken a year, is our investment in customer service. A year ago there were just 12 people in a conference room doing call-center work. Today we have 64 people in a call center doing inbound customer service.

So why haven’t additional peer to peer lending platforms launched?

That’s the second part to your previous question. The first part is, and let’s be clear, our competition is quite broad. The second part is, as I mentioned earlier, this business is complex. Getting the credit modeling right is very hard. Getting the consumer marketing piece right is very hard. And when I say hard, I do not just mean that it takes extra work. It also requires a team of incredibly smart people.

It is a ton of work in a lot of different directions, all very complex.

Look at Lending Club and Prosper: hundreds of millions of dollars have been invested just in this peer to peer space. It is platform business, so you have to have great technology. You have to register state by state. You have to get the SEC to sign off. It is a ton of work in a lot of different directions, all very complex.

The regulatory and legal piece is actually huge. There is an extra barrier, which is that the SEC has actually not approved anybody to do peer to peer lending other than Lending Club and Prosper. And I believe that is because the volume of information we send those guys is impossible to get through. We file hundreds of S-1s on loans every day. Why would they want to create that much more work?

I think it has been really hard for anyone else to build a scalable business. Look, this company has worked since 2006 to get there, and that success is why Prosper has value.

It’s worth remembering that there are plenty of companies in the consumer credit space, they just don’t look like Lending Club or Prosper. There is SoFi, OnDeck, Kabbage, LendUp, and so on. Everyone is trying to find a way into the larger category of unsecured consumer credit. OnDeck and SoFi are basically using their balance sheet to buy loans. SoFi is securitizing them and rebuying, so they have a sort of hybrid model. OnDeck is using their own capital.

One of the things that makes Prosper so unique is that, unlike a bank, we use institutional and retail borrowers. We are not capital constrained. So as we grow, we do not have to keep going out and raising more money. We simply bring customers on board.

You guys do seek out rounds of investor funding.

We do for operating capital. Companies like OnDeck and SoFi raise money to invest in loans.

What is the danger of a platform like Lending Club expanding from personal loans into small business loans?

Small business lending is a completely different credit model. It is a different borrower with different underwriting. I’m not going to criticize it, but Prosper already has a very good credit model that works, which is probably the most important thing that we do. Our job is to make sure we are pricing the loans correctly and estimating the net-loss charge offs so that investors can make an informed decision. If we do that wrong, it’s over.

So if we have a credit model that works for unsecured personal loans, you can’t just apply that to business loans. Business loans involve both the business and a person. You have receivables. The loan uses a fundamentally different credit model. Yes, you can earn a higher return, but you can also lose your shirt. If you look back in history, a lot of companies that got good at this went into that, and that exact thing happened to them.

Philosophically, I believe in sticking to our knitting. We are in a huge addressable market, and our point of differentiation is that we are going to be the best in the business of personal loans.

Regarding the tremendous rate of growth within consumer lending, it seems en route to interact with the wider American story at some point. What does a platform like Prosper look like when it becomes a staple of national finance?

The longer-term vision for us is to change the way people experience access to credit. So, rather than going to a bank and explaining yourself, rather than having to wait three weeks to get an appraisal, we really want to create an easy, understandable customer experience. There are brands that we admire whose purpose is to simply delight the customer, to positively surprise people and treat them with respect, and that is kind of what we are trying to go after in financial products. I think it is a clear point of differentiation from the way the credit cards and the banks have treated consumers.

I just took an Uber car to get here this morning, and was pleasantly surprised when they asked me if I wanted a bottle of water.

Living in San Francisco, I have had time to look at that company. What is so cool is that, when you are an Uber driver, you go to training and they say, “Differentiate yourself from a taxi. This is not a taxicab. Offer people some water.”

To that point, 51% of our loans fund in two days. You experienced the speed with which our loans fund when you got a loan for yourself. We are now averaging three days to fund per loan. Philosophically, Prosper is focused on the borrower experience, and we want people to be delighted by their experience here.

LendingMemo aims to be an education hub for self-directed retail investors, focusing on the way peer to peer lending empowers average folks to get their hands dirty with their own investing and pull out a great return. What will the lender picture look like in 10 years?

I would like to see retail investors, whether it was high net-worth or actual retail, be 50% or more of the platform. I truly believe that, in order to make this a 100-year company, this has to happen. I mentioned this on the Prosper blog, but if you look at where we are right now, last year was about survival. Survival meant proving to the world that you can profitably originate loans, acquire borrowers, and fund the loans.

Let me give you the context. In October or November 2012, Prosper had a single user who was funding a massive piece of the loans on the platform. The company had started to spend a lot of money on marketing, was bringing in loans, but this user suddenly dropped off the platform. So all these loans, all that money they spent, died on the vine, and the company was shell-shocked.

Our team came in here and said, “Let’s clean up the corporate structure, and then go out and create lender stability.” That meant putting in place a bankruptcy remote and addressing this class action lawsuit. It meant cleaning up the bank structure stuff and making sure the backup servicer was in order.

The previous backup servicer wasn’t in order?

It was, but now we have a hot backup instead of a cold backup. If the company went out of business, the previous servicer would have to ramp up. Our new servicer is already running. From a risk perspective, that is a big difference.

Huge. It’s reassuring to investors.

Right. So we cleaned up this corporate mess, and then we went out and created lender stability. We said, “Let’s bring on some institutions. We need to know that if we go out and spend millions of dollars on finding borrowers that the loans will get funded.” So we brought on a couple of partners and went off to the races. Last year was about creating that proof.

We have not added a single new institutional lender to the platform this year. (We are adding one, but it is a AA-grade buyer, a bank, because AA-grade loans are not getting funded very quickly.) Back to your question on our lender environment, our stability and growth has allowed Prosper to now begin focusing on retail. We are growing really quickly, are poised to issue over $100m per month by May. So if retail shows us it has the headroom to grow, then we don’t have to add institutional lenders. If it doesn’t, then we have add institutional dollars to soak up the extra demand.

Perhaps one thing to keep in mind, and you probably know this better than myself, but retail investors seem like they’re a romantic bunch. It may take a while to get them on board, but then they stick with you. I guess I just wouldn’t expect mom and pop investors to quickly jump into sudden loan availability.

Right, but we want to create an environment where they can start coming in, giving it headroom to see where it goes. Remember that we have retail, high net-worth investors, hedge funds, banks, and BlackRock. BlackRock, the world’s largest asset manager with $4 trillion, is interesting because they are a kind of hybrid. They are investing their client portfolios into the funds that own the loans, so they are going to be a little stickier. But hedge funds, if the climate changes, may be gone. A lot of these other guys have leverage, and the leverage providers are all the same people, and that creates correlation. If one bank says it is done, then everybody using that bank is done as well.

That is why retail investors are so important.

That is why retail investors are so important. That is why Prosper is committed to find more retail platforms to come on here, whether it is through wealth management or something else. But it’s also important to state how hard it is to go out with a sales force and market $5,000 investor accounts. It just doesn’t scale.

That makes sense. I guess I’m just interested in what a mature retail-investor platform looks like perhaps 10 years down the road.

Prosper, ten years from now, is going to be a multi-billion dollar company investing in a diverse set of financial products. Retail investors would be investing in the product set that is currently only available to banks, card issuers, and debt issuers. We could have mortgage loans, auto loans, personal loans — the whole suite, and actually have it funded by the world instead of large pools of capital that are captive to these companies.

Really, that is the overarching goal here. The thing that scares the banks is that this is a disruptive disintermediation of their capital consolidation – it is the democratization of credit. And I would love to see that. It would be really cool. The returns that people can earn on those products, if they are constructed properly, could be a suite of investments that none of us have access to today. This is an idea whose time has come.

But it’s still complex. If you think about the way that Prosper worked when Chris Larsen started the company, it was like eBay for credit. But I think it was proven pretty quickly that, while free markets are good for pricing many things, us as lay people (and I would put myself in that group) are not good at pricing credit risk. So this has to be a mediated platform. If you put somebody like Prosper in the middle, and you can actually have a bank without a bank, and that is what we are building today.

For couple of now my Prosper filters have been producing zero results. I wrote them twice, first time receiving no response, and the second time (about two weeks ago) they responded that it is a known problem that they are working on. Still, nothing has changed.

Anyone else having this problem? I’ve quit adding more funds and thinking about withdrawing everything as it comes available–this is not inspiring confidence at all.

Is this the same man who owns merlin securities(Online Hedge funds management program)?